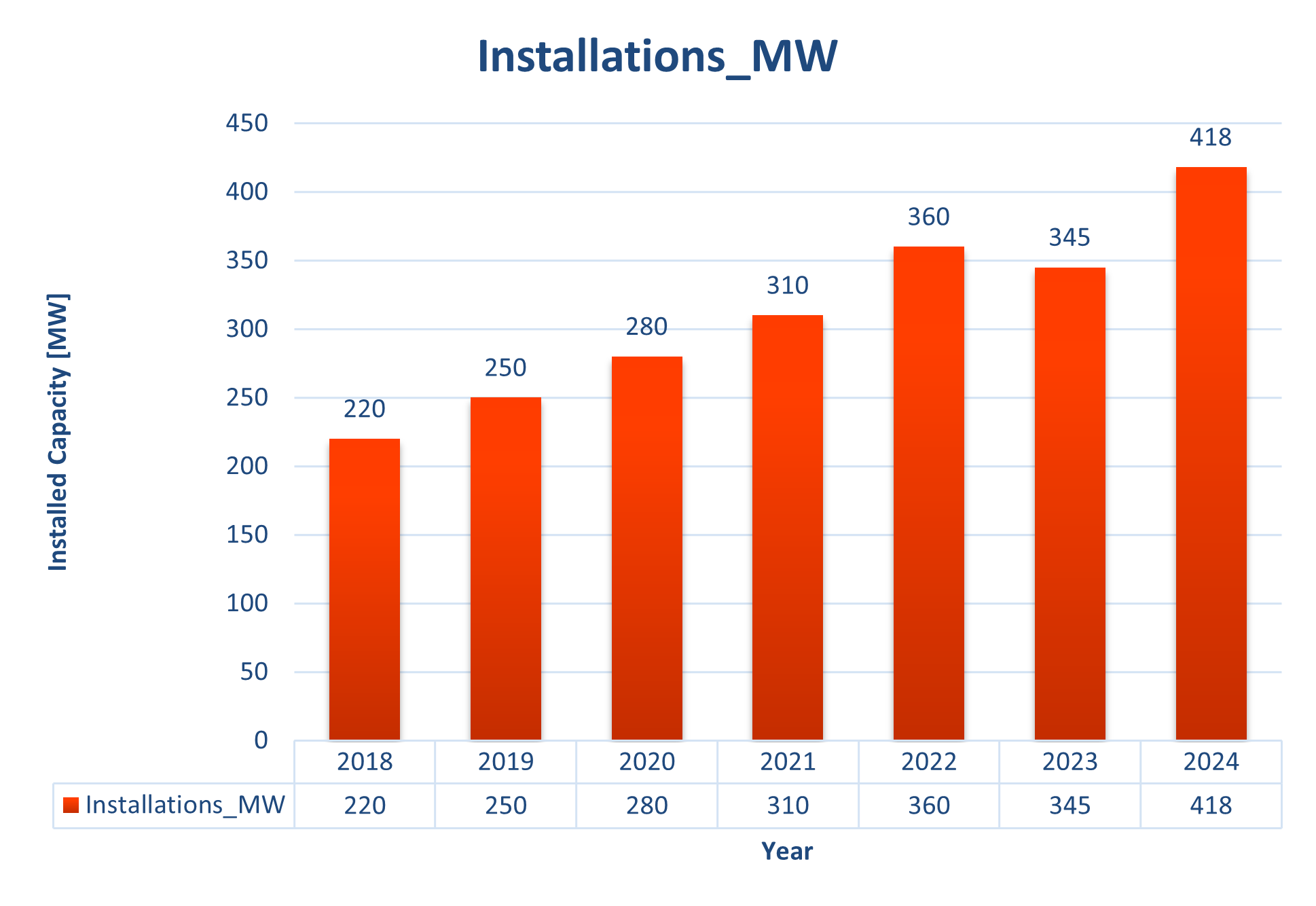

Stationary fuel cells are deployed across a wide range of applications, from residential micro-CHP systems to multi-MW prime power and utility-scale plants. Based on the latest AFC TCP data, global installed stationary fuel cell capacity increased from ~220 MW in 2018 to ~345 MW in 2023, with a 2024 forecast of ~418 MW (corresponding to ~8–10% CAGR over 2018–2024). Stationary systems represent ~15% of total fuel cell MW deployed in 2022–2023.

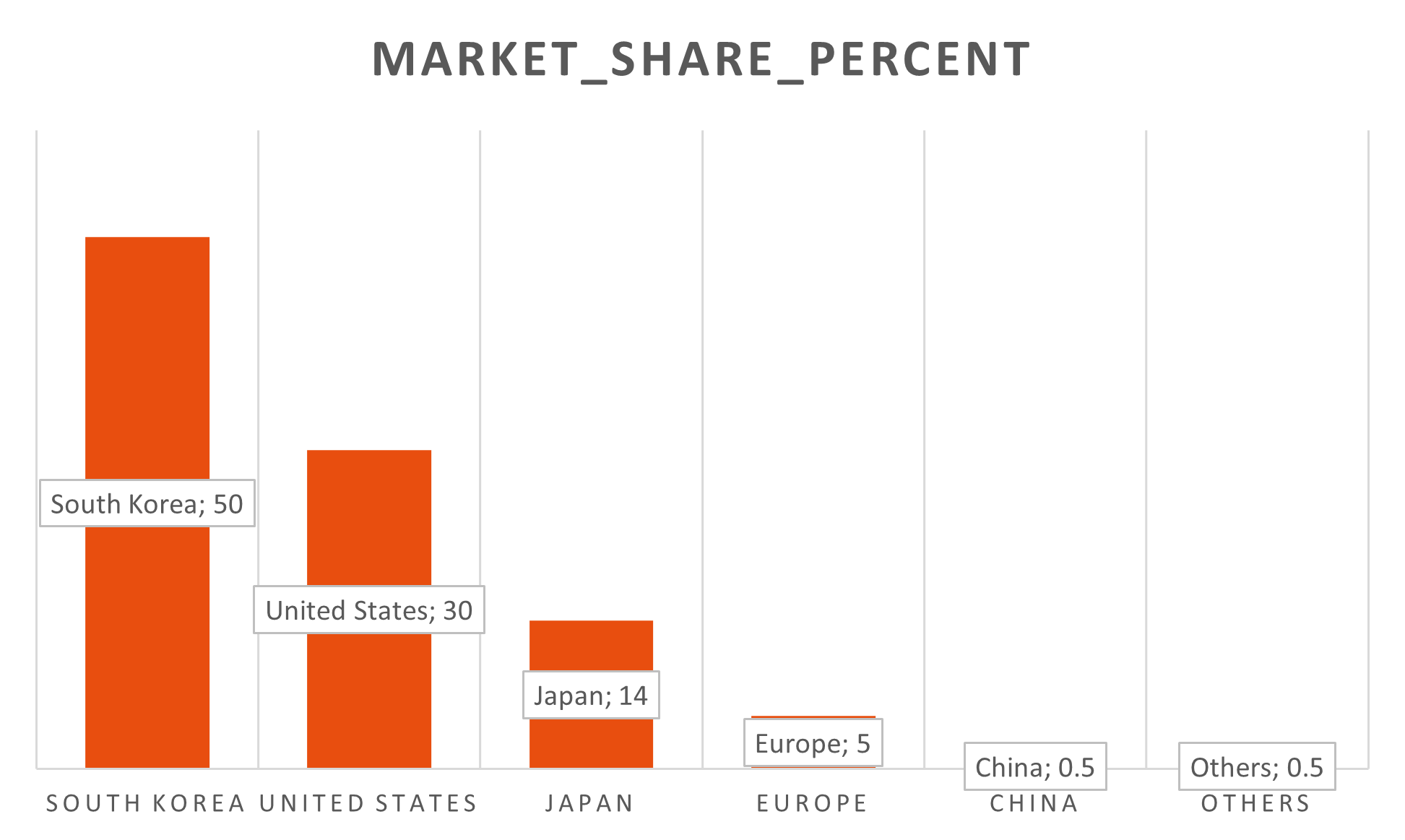

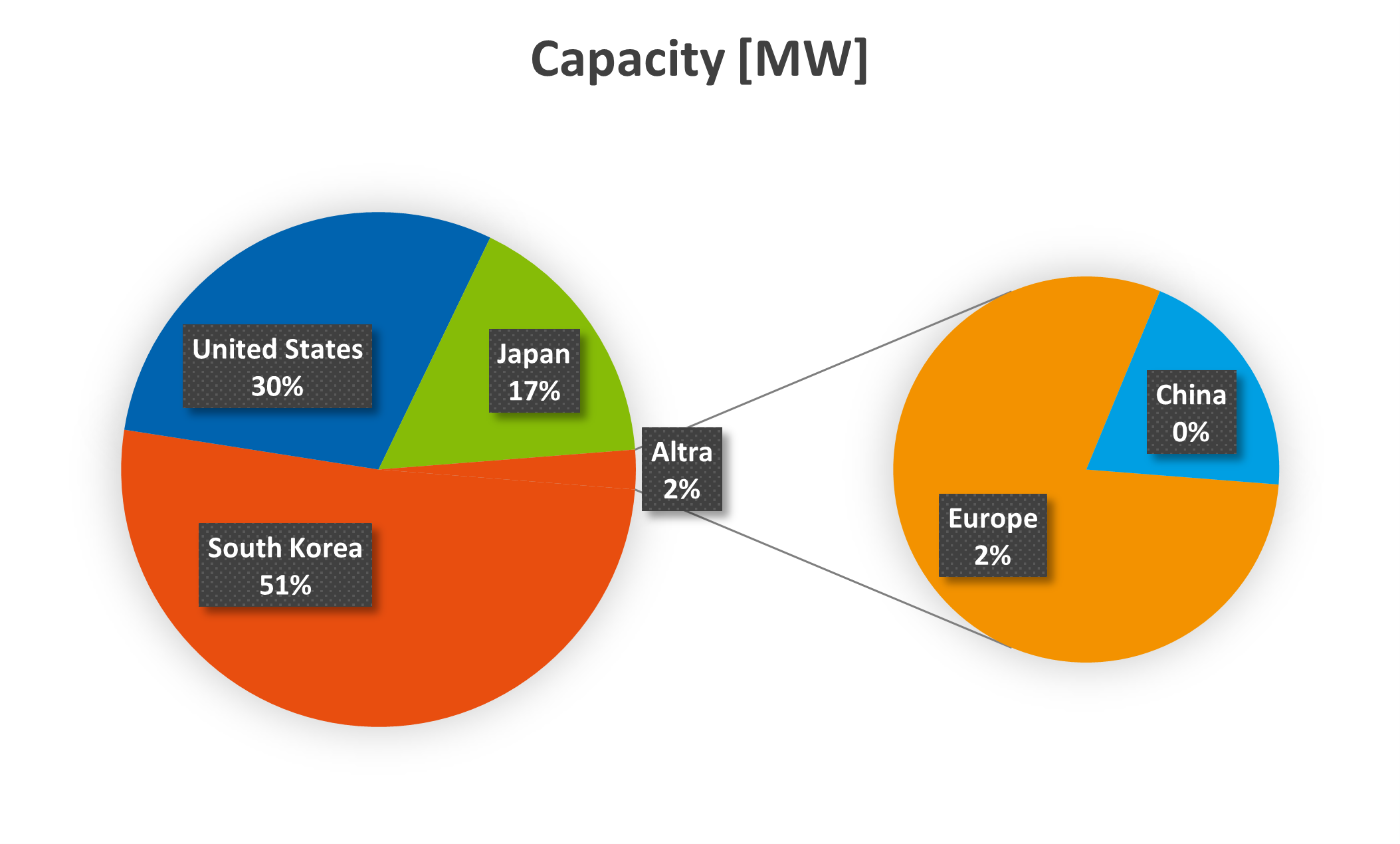

Regionally, South Korea remains the main market by installed capacity (>1 GW), followed by the United States (~600 MW) and Japan (~336 MW). Europe (~40 MW) and China (<20 MW) currently contribute a smaller share, although China shows the fastest long-term growth forecast.

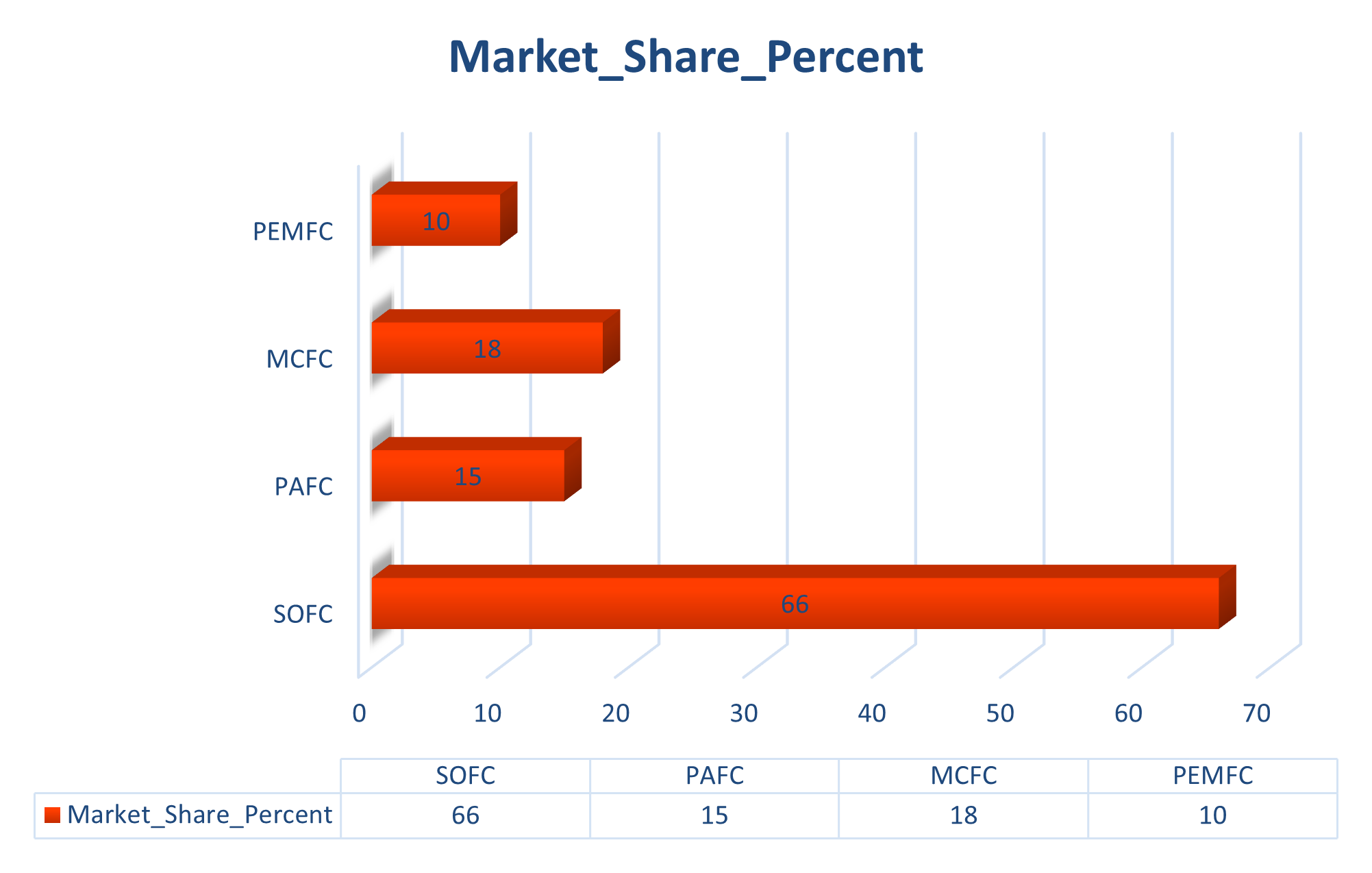

In terms of technology, SOFC accounts for ~two-thirds of stationary MW (prime power, grid support), while PAFC (~15%) and MCFC (~15–18%) remain important for large CHP and multi-MW systems; PEMFC contributes ~10% of stationary MW, mainly in micro-CHP and backup/critical power.

Installed capacity rises from ~220 MW (2018) to ~345 MW (2023), with ~418 MW expected in 2024.

South Korea leads (>1 GW), followed by the United States (~600 MW) and Japan (~336 MW); Europe (~40 MW) and China (<20 MW) have smaller installed bases.

SOFC ~66% of stationary MW; PAFC ~15%; MCFC ~15–18%; PEMFC ~10%.

Residential micro-CHP (Japan, Europe); C&I prime power (USA, South Korea); backup/critical power (telecom/data centers, mainly small PEM systems); utility-scale power plants (10–80 MW, South Korea/USA).

Secretariat Technology Collaboration Programme on Fuel Cells and Electrolyzers

Marietta Sander

CAMPUS TÜV NORD GROUP

Am TÜV 1

45307 Essen

Germany

Mobile: +49 171 865 0862

E-Mail: secretariat@ieafuelcell.com

© 2026 Fuel Cells and Electrolyzers Technology Collaboration Programme In association with IEA 🔶 Web Design by Klicklounge